Video Conferencing

Video communication apps allow two people in different locations to communicate face to face. As 3G and 4G technology availability has made connection faster and cheaper, video chat has become very popular across generations. Video conferencing is more than a Skype chat with Grandma. It also provides the ability to share educational information and provide a platform for business negotiations.

That’s one of the big differences between video conferencing and video banking – the former enables communication between businesses and is not addressing the consumer side of collaboration. Additionally, most video conferencing platforms require both parties to set a date and time to communicate, which creates service friction. How many times have you been the only one to show up for a video conference? It’s incredibly frustrating; imagine experiencing that as a consumer.

Video chat apps aren’t secure enough for banking transactions. You’ve probably heard the recent news about the iPhone FaceTime bug that allows users to eavesdrop on others before they even accept the call. The last thing your FI needs is bad publicity suggesting you don’t properly safeguard financial information because you used FaceTime to conduct financial transactions.

Finally, video conferencing’s main purpose is cost savings. It means you don’t have to fly your vendor or your remote team members into the main office for an in-person meeting. Free or low-cost video conferencing services might be cheaper than video banking, but when it comes to digital channels, cost savings isn’t the only factor to consider. Convenience, consumer experience, compliance, and workflow must be included in your due diligence.

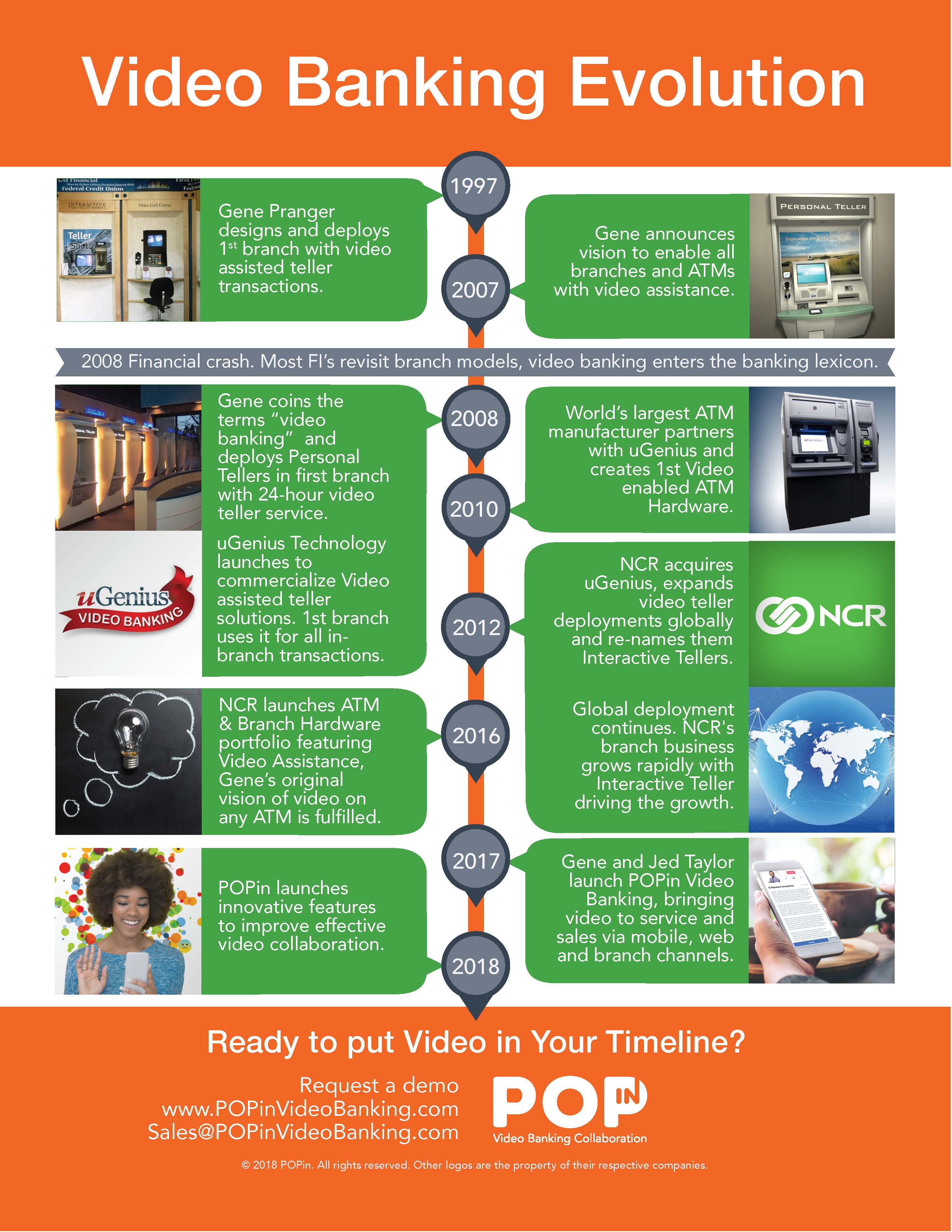

Video Banking

Video banking, on the other hand, does more than allow face-to-face digital communication. It recreates an entire branch experience, with tellers, consumer service representatives, loan officers, and financial advisors.

That’s the biggest difference between the two channels – video banking was custom built to meet the needs of banking consumer needs and work with banking workflows. Unlike video conferencing, video banking usually includes the following features:

- Document collection

- Document signature

- Screen sharing

- Presentations

- URL sharing

- Standardized business workflows

- Branch, web, and mobile deployments

A robust video banking app brings all of your products and services together, which increases your staff efficiency and racks up sales.

Unlike video conferencing, which requires everyone to show up at a specific date and time, video banking can be built into your call center queue. That makes it on demand for consumers, the way retail channels should be.

Video banking also allows you to record the call, produce logs and metrics to track performance and provide data to prove compliance. That’s important: video banking apps are compliant with security regulations that safeguard financial data. WebEx and FaceTime are great services, but they aren’t going to impress your executive team.

Financial regulators are expected to scrutinize technology even more in 2019, according to a recent American Banker article. It reported that because Democrats have regained control of the House, and Republicans only hold a slim majority in the Senate, banking regulation is expected to tighten. Additionally, banking regulators are still under pressure to protect consumers from data breaches. You should expect your examiner to review all of your fintech vendors and digital channels, searching for weak links. Now is not the time to skimp on security!

Finally, consumers value experience more than ever. In fact, surveys keep revealing that younger consumers are willing to pay more for a loan if the lender provides a superior digital experience. Even Grandma, who already knows how to use video chat technology, appreciates the convenience video banking provides – many banks and credit unions have found that video banking adoption rates across all generations have been higher than expected.

The differences between video conferencing and video banking are clear. Start providing better experiences, that will make your financial institution one your consumers love.